Minimum Volatility Portfolio

In our active risk-controlled strategies, we generally observe a negative relationship between return and various risk measure. It is therefore not surprising to see this effect in diversified portfolios leading to Minimum Variance portfolios outperforming traditional benchmarks.

What's New:

More Educational Content coming soon

More educational content

to come. Sujects include double taxation of bonds and corporate governance.

More educational content

to come. Sujects include double taxation of bonds and corporate governance.

April 19, 2012: Death of a great investment counselor, Carl H. Otto

Updated: April 20, 2012

Minimum Volatility Portfolio

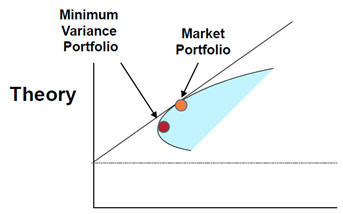

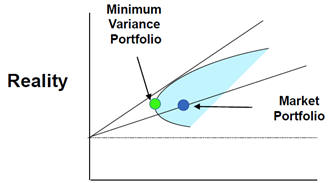

It is generally agreed by financial market participants that you get compensated more for taking more risk. This is why you expect to earn more in equity investments than fixed income investment – at least in the long run.

Yet quantitative / behavioral finance researchers (including myself) have often noted the negative premium attached to bearing more risk within the equity market. All quantitative / behavioral portfolio managers have been exploiting this apparent anomaly to some extent. In fact, we observe that the market portfolio is not on the efficient frontier:

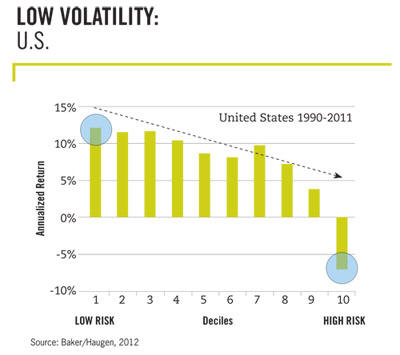

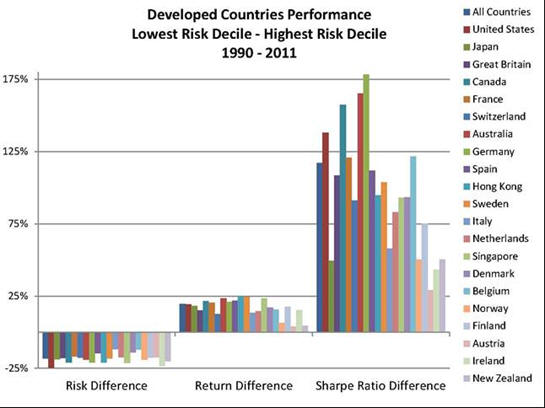

Numerous papers have been written on the subject. In particular, the paper by Narin Baker (Guggenheim Partners) and Robert Haugen on “Low Risk Stocks Outperform within All Observable Markets of the World”, April 2012. They measured trailing 24-month volatility from 1990 to 2011 to rank stocks into deciles, quintiles and halves. This is repeated for the whole backtest period. The results are clear:

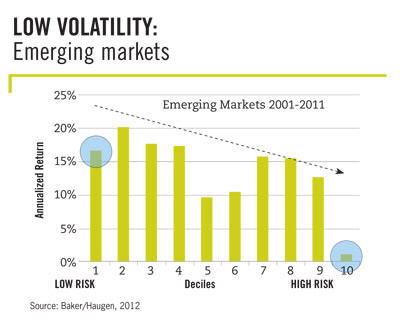

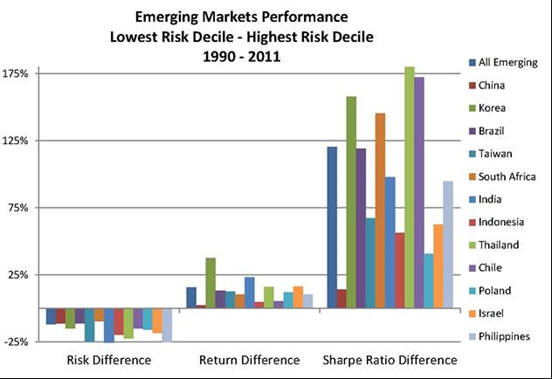

and in emerging markets:

In their study, they analyzed 21 developed countries and 12 emerging market countries. They observed a significant risk reduction in each country, a significant return enhancement in each country, leading to a very significant Sharp ratio enhancement.

and similarly for emerging markets:

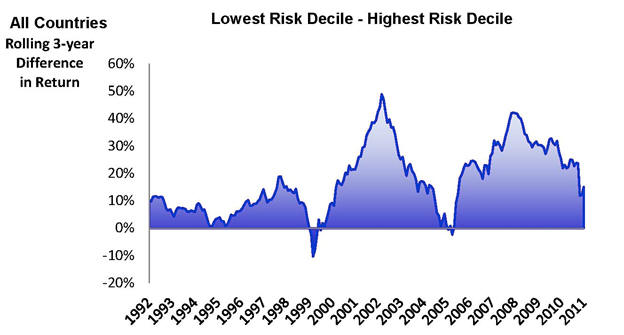

Low risk stocks do not outperform all the time. But on a rolling 3-year basis, from 1990 to 2011, low risk stocks had very few periods of underperformance.

With the growing evidence of the superior return to risk profile of low volatility stocks, it is not surprising to observe an increasing demand for and supply of low volatility products. All low volatility portfolios are not created equal though. Some use very simple approach while others use more sophisticated ones.

Some approaches use volatility, other use beta to represent risk. The portfolio construction approach can substantially diverge too. Some use simple screen-based/ranking-based approaches while other used mean-variance optimization-based approaches.

Volatility and beta measures

Volatility and beta can be calculated over different periods ranging from 12 months to 60 months. From a statistical point of view, the shorter the period, the noisier (less precise) the estimate. But the longer the period, the less relevant the estimate can be if the company changed over the period of estimation.

It is well known that small cap less liquid stocks do not trade as frequently as larger liquid stocks. This nonsynchronous trading effect causes all risk measures like volatility, beta, correlation to be significantly underestimated. This underestimation effect is also present and well documented in illiquid asset classes like real estate and private equity and to some extent in many hedge fund strategies. Therefore:

- volatility and beta are well estimated for liquid stocks

- volatility and beta are underestimated for less liquid stocks

If we rank stocks based on such risk measures, the stocks with the underestimated risk measures will show further down such ranking. Part of such apparent low volatility effect may well be due to the neglect effect where stocks that are not followed by many analysts (or not followed at all) may hide some gems which will return more than their peers. Yet we will see in a moment that low volatility portfolios tend to be larger illiquid stocks.

There exists a simple statistical procedure to adjust the underestimation of traditional risk measures but it doesn’t seem to be used by most investors.

Volatility and beta estimates from risk-factor model, when properly estimated, do not suffer from this underestimation effect.

Ranking-based or Screening-based portfolio construction

Ranking-based approaches to portfolio construction have been used for a very long time. On the positive, they are extremely simple to use and do not require advanced expertise and technology. On the negative, they do not allow for real risk controls as they are a one factor (or a composite factor)-based approach. Ranking-based approaches do not take into account covariances between stocks in building a low volatility portfolio – yet every professional investor understands the benefit of diversification in lowering risk at the portfolio level.

Equal-weighting or risk-weighting

Ranking or screening provides a list of candidates stocks to include in a portfolio. Such screening needs to be combined with a system to weight stocks. Various ad-hoc weighting schemes are used with the most popular being equal-weighting and inverse of volatility weighting. Both approaches will bias the portfolio toward smaller caps stocks within the screened set of stocks. The inverse of volatility weighting scheme will tend to overweight stocks with underestimated risk measures generally linked to trading illiquidity.

Minimum Variance portfolio construction

While minimum variance could be used with historical risk measures which suffer from the non-synchronous trading/underestimation effect mentioned previously, it is generally used with predictive factor model which are less negatively affected with this problem.

Minimum variance makes full use of covariances between stocks in building its lowest volatility portfolio. It is also a very flexible portfolio construction approach which allows for constraining various aspects of the portfolio to achieve greater customization or to take into account some known weakness of the risk model.

Time variation

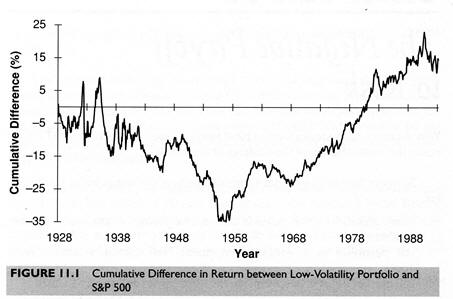

The low volatility anomaly has been going on for a long time but it was not always like this. In his book “The Inefficient Stock Market” Robert Haugen showed that from 1928 to 1958, Low volatility stock underperformed the S&P 500:

Since the beginning of the 1960s, low volatility stocks outperformed the S&P 500. One of the main factors explaining this is the increased importance of institutional investors. This could also be linked to the increased popularity of indexing with large institutions buying large amounts of index products and not trading them afterward.

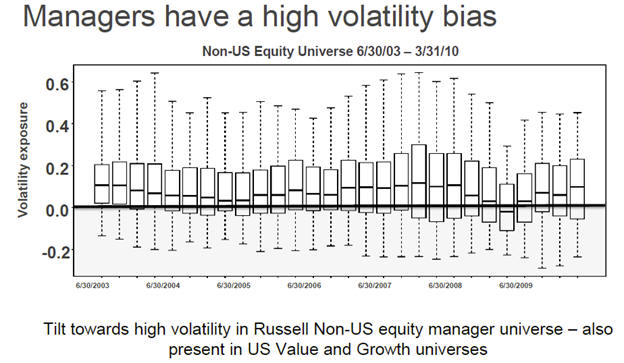

Active managers generally do not try to add value with low volatility stocks as they offer less return enhancement potential. Russell documents a significant tilt toward volatile stocks in their active managers’ universe:

Is this really a low volatility effect?

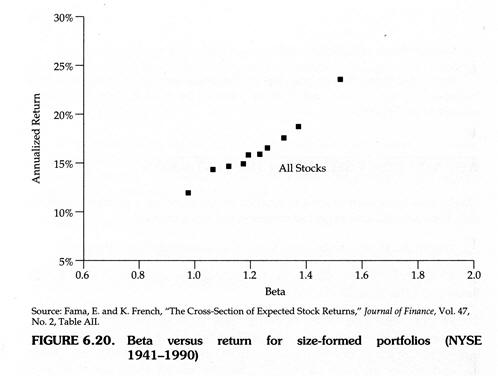

Fama-French grouped stocks by size decile. They noted that the first (large caps) decile has a Beta lower than one and that the betas of the smaller capitalization stocks increase with size. They observed the following expected pattern between return and size decile with the smaller/riskier stocks returning more over the 1941-1990 period. Thus riskier stocks (when ranked by size decile) returned more as predicted by the theory.

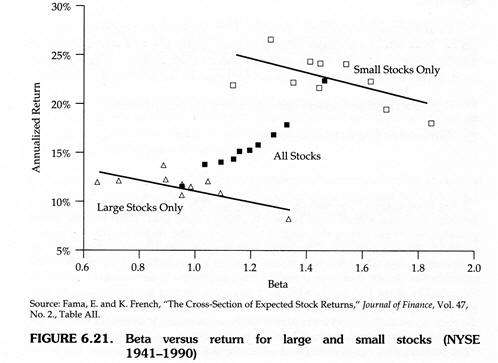

But within each decile grouping, he observed a negative relationship between return and risk:

Taking into account the time variation effect discussed previously, we conclude that to properly model this anomaly, we may need to properly model this time variation together with the interaction effect between size and risk…

What else do we have?

Guggenheim Partners document the following style exposure in 10 international markets:

- Low volatility stocks have a higher average market cap

- Low volatility stocks have a lower average sales growth

- Low volatility stocks are less liquid

- Low volatility stocks are cheaper as they have lower P/E ratios

- Low volatility stocks have higher average profit margins

- Low volatility stocks have a higher average dividend yield

While the large cap bias is a bit surprising, the value and illiquidity bias is not as these two are linked to higher returns in the long run. The low volatility anomaly may in fact be the realization of the illiquidity and value premium.

CONCLUSION

Low volatility portfolios tend to have the following characteristics:

- Larger caps

- Less liquid stocks

- Value bias

- Slower growth

- More profitable firms

The apparent outperformance of low volatility stocks is time varying and there is some interaction with the size of firms. The apparent anomaly may be linked to increased ownership by large institutional investors and the increased popularity of indexing. The increased supply and demand for such products may change the return behavior of this apparent anomaly. This is why some firms do not sell it as a return enhancing product but rather as a volatility reducing product. In fact, this is the only property that we can guarantee for the future!

For more information on the low volatility strategy and how to exploit its time varying nature and its interaction effect, please contact us.

Dominic Clermont, ASA, MBA, CFA